AARP secondary insurance to Medicare offers additional coverage that complements your existing Medicare plan. Discover how this insurance can benefit you in unexpected ways as we delve into the details below.

Exploring the eligibility criteria, coverage details, cost, enrollment process, and customer experiences will shed light on the advantages of having AARP secondary insurance alongside your Medicare plan.

Introduction to AARP Secondary Insurance to Medicare

AARP secondary insurance to Medicare is a supplemental insurance plan offered by the American Association of Retired Persons (AARP) to provide additional coverage beyond what Original Medicare offers.

Complementing Medicare Coverage

AARP secondary insurance complements Medicare coverage by filling in the gaps left by Original Medicare, such as deductibles, copayments, and coinsurance. This additional coverage can help reduce out-of-pocket expenses for healthcare services not fully covered by Medicare.

Benefits of AARP Secondary Insurance

- Provides coverage for services not covered by Medicare, such as dental, vision, and hearing care.

- Offers peace of mind by reducing out-of-pocket costs for medical services.

- Allows beneficiaries to choose their healthcare providers without network restrictions.

- Includes additional benefits like fitness programs, wellness resources, and preventive care services.

Eligibility Criteria

To qualify for AARP secondary insurance to Medicare, individuals must first be enrolled in Medicare Part A and Part B. This means that they must be at least 65 years old or have a qualifying disability. AARP secondary insurance is designed to supplement the coverage provided by original Medicare.

Comparison of Eligibility Criteria

- Medicare: Eligible individuals include those aged 65 and older, younger individuals with certain disabilities, and people with end-stage renal disease.

- AARP Secondary Insurance: Requires individuals to be enrolled in Medicare Part A and Part B, regardless of age or disability status.

Specific Conditions for AARP Secondary Insurance

- Enrollment in Medicare Part A and Part B is mandatory.

- Individuals must maintain their Medicare coverage to remain eligible for AARP secondary insurance.

- Some AARP secondary insurance plans may have additional eligibility requirements based on the specific plan chosen.

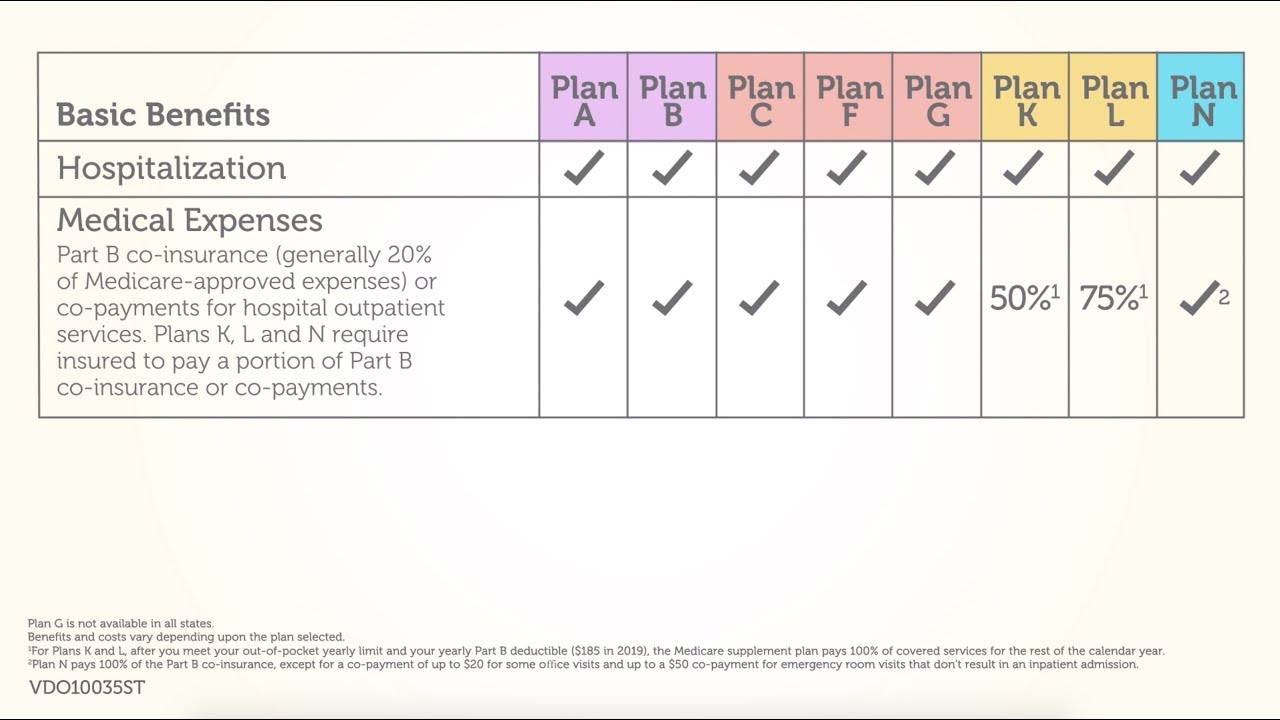

Coverage Details: Aarp Secondary Insurance To Medicare

When it comes to coverage details, AARP secondary insurance offers a range of services and expenses beyond what Medicare covers. This additional coverage can help alleviate financial burdens and provide peace of mind for individuals enrolled in Medicare.

AARP secondary insurance covers services such as:

- Hospital stays

- Skilled nursing facility care

- Home health care

- Medical supplies and equipment

- Preventive services

- Prescription drugs

However, it’s important to note that there are limitations and exclusions in the coverage offered by AARP secondary insurance. Some services or expenses may not be covered, so it’s essential to review the policy details carefully to understand what is included and what is not.

Additionally, AARP secondary insurance can help with out-of-pocket costs not covered by Medicare. This can include deductibles, copayments, and coinsurance that Medicare beneficiaries would otherwise have to pay on their own. By providing supplemental coverage, AARP secondary insurance can help individuals manage their healthcare expenses more effectively.

Cost and Enrollment

When considering AARP secondary insurance to Medicare, it is essential to understand the cost structure and enrollment process involved. Below, we will detail the cost structure of AARP secondary insurance, provide information on how to enroll, and compare the enrollment process for both Medicare and AARP secondary insurance.

Cost Structure of AARP Secondary Insurance

- AARP secondary insurance to Medicare typically involves monthly premiums, deductibles, copayments, and coinsurance.

- The cost may vary depending on the specific plan chosen, coverage options, and the individual’s location.

- It is important to carefully review the cost details of each plan to determine the best fit for your healthcare needs and budget.

Enrollment in AARP Secondary Insurance

- To enroll in AARP secondary insurance, individuals must first be enrolled in Medicare Part A and Part B.

- Once eligible, you can visit the AARP website or contact their customer service to explore available plans and enroll in the one that suits your needs.

- Enrollment periods may vary, so it is crucial to stay informed about enrollment deadlines and any special enrollment periods.

Comparison of Enrollment Process, Aarp secondary insurance to medicare

- Enrolling in Medicare involves signing up through the Social Security Administration, either during the initial enrollment period, special enrollment periods, or the general enrollment period.

- On the other hand, enrolling in AARP secondary insurance requires being enrolled in Medicare first, followed by selecting and enrolling in an AARP plan separately.

- Both Medicare and AARP secondary insurance have specific enrollment requirements and deadlines that individuals need to adhere to for coverage.

Customer Experience

When it comes to customer experience with AARP secondary insurance to Medicare, it is essential to hear from individuals who have actually used the service. Their testimonials and reviews can provide valuable insight into the benefits and potential drawbacks of this insurance option.

Testimonials and Reviews

- One satisfied customer mentioned that AARP secondary insurance provided comprehensive coverage that gave them peace of mind in managing healthcare costs.

- Another individual praised the customer service representatives for being knowledgeable and helpful in navigating the enrollment process.

- Some users have highlighted the convenience of having AARP secondary insurance in addition to their Medicare coverage, making it easier to access a wider range of healthcare services.

Common Feedback and Complaints

- Some users have expressed concerns about the cost of AARP secondary insurance, particularly if they are on a fixed income and looking to manage healthcare expenses effectively.

- A few individuals have mentioned delays in claims processing, leading to frustration and inconvenience in accessing timely healthcare services.

- There have been occasional complaints about limitations in coverage for certain procedures or treatments, prompting users to explore alternative insurance options.

Tips for Maximizing Benefits

- Regularly review your coverage details to ensure you are aware of any changes or updates to your benefits under AARP secondary insurance.

- Take advantage of wellness programs and preventive care services offered through AARP secondary insurance to maintain your health and well-being proactively.

- Reach out to customer service representatives for any questions or concerns you may have about your coverage, eligibility, or claims process to receive prompt assistance and guidance.

Last Point

In conclusion, AARP secondary insurance to Medicare provides a valuable safety net, enhancing your healthcare coverage and reducing out-of-pocket expenses. By understanding the benefits and nuances of this insurance, you can make informed decisions to secure your healthcare needs.

FAQ Overview

What are the eligibility requirements for AARP secondary insurance to Medicare?

The eligibility criteria typically involve being an AARP member and already enrolled in Medicare Part A and Part B.

What services are covered by AARP secondary insurance in addition to Medicare?

AARP secondary insurance may cover services like vision, dental, and hearing aids, which are not included in original Medicare.

How can I enroll in AARP secondary insurance?

To enroll, you usually need to contact AARP directly or visit their website to complete the enrollment process online.